Reading a release sheet, floor by floor

Why a 47th-floor unit can cost more per square foot than a 49th-floor unit in the same line, and what the discontinuities in a developer's pricing tell a buyer about the building.

By Fernanda Zomignani

A developer's release sheet for a Miami pre-construction tower is a single spreadsheet. Rows are unit lines. Columns are floors. Cells are prices. The pattern across the cells is the developer's view of the building.

A buyer who has only seen public price lists assumes the per-floor escalation is continuous and linear. It is not. The release sheet contains five discontinuities that the public list flattens. Each discontinuity tells the buyer something specific about the building. Reading them is the difference between negotiating against the developer's actual structure and negotiating against the marketing version of it.

This essay walks through the five discontinuities, what each one means, and how a buyer who understands them changes the negotiation.

The base assumption: one to two percent per floor

The release sheet starts from a base. Each floor adds a vertical premium of one to two percent above the floor below. The premium funds the view that opens as the unit rises above adjacent buildings. The math is consistent across South Florida high-rises and reflects the long-established correlation between elevation and resale value.

Inside a forty-story tower, this base premium compounds. A unit on the thirty-fifth floor of a given line typically prices at one and a half times the same unit on the fifth floor, against the floor premium alone. The compounding is the structural reason that the lower floors of a tower are priced as the entry product and the upper floors as the flagship product.

A buyer who is comparing two units of the same square footage across twenty floors of separation is comparing two different products inside the developer's pricing model, even if the brochure copy is identical. The square footage is the same. The view is not. The pricing is not.

This is the base. The five discontinuities are where the base breaks.

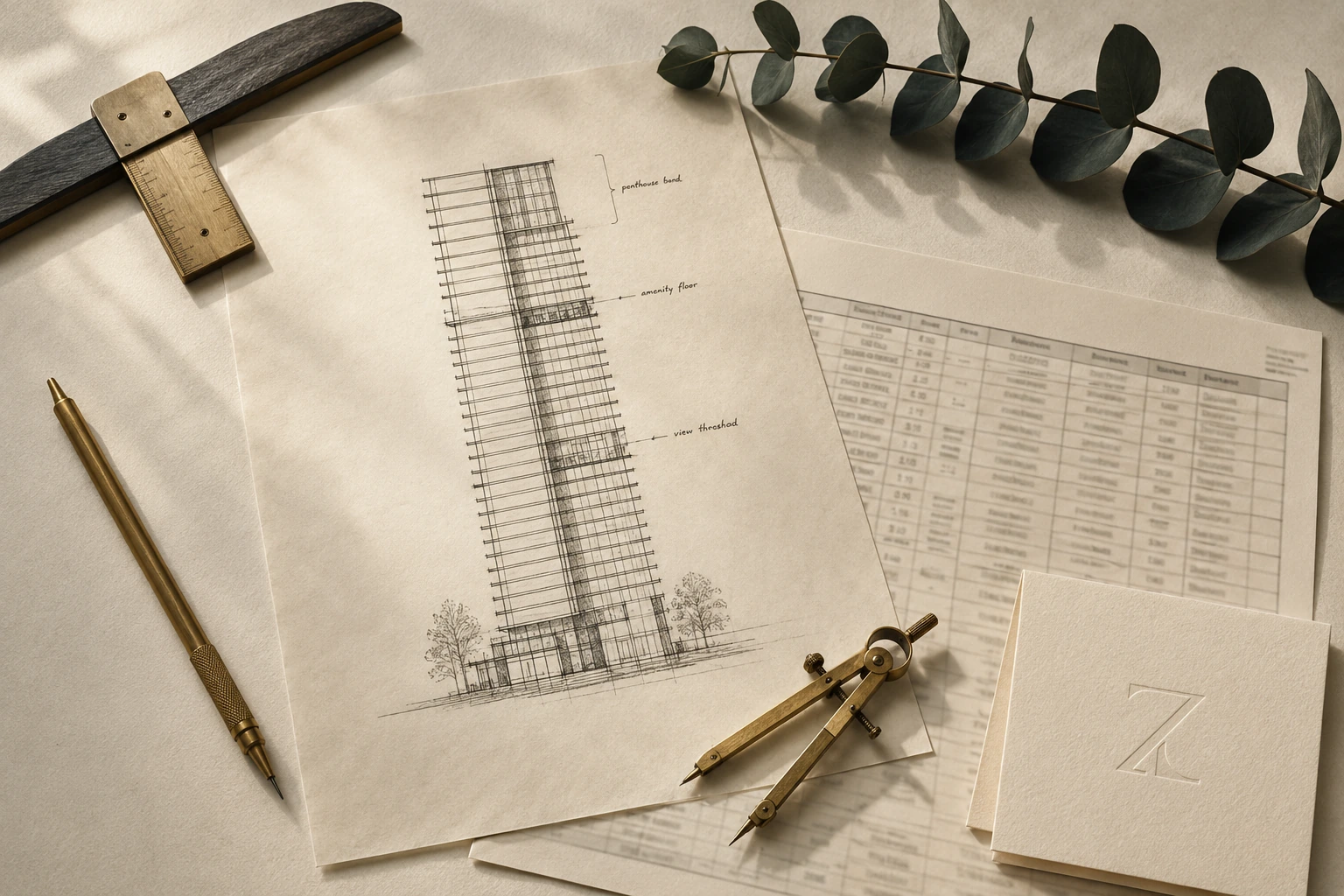

Discontinuity one: the view threshold floor

Every tower has a floor at which it clears its neighboring rooflines. Below that floor, the view is partial, occluded by adjacent buildings, parking structures, or the lower portions of nearby towers. Above that floor, the view is the marketing view: water, skyline, horizon.

The developer knows where that floor is. The release sheet shows it explicitly. The premium between the floor immediately below the threshold and the floor immediately above is typically four to six percent, not the one to two percent that applies elsewhere. The discontinuity is the developer's quantification of the view itself.

A buyer who is choosing between two units that straddle the threshold is making a decision that is meaningfully larger than the floor number suggests. The unit below the threshold is priced against a residential view. The unit above is priced against the building's marketing view. The resale market will read the same distinction.

On the public list, the threshold is invisible. The asking prices appear to follow a continuous escalation. The discontinuity is hidden inside the per-floor pricing. Only by looking at the release sheet does a buyer see where the threshold is. Where it is varies by tower. A buyer comparing two Brickell projects with similar square footage and similar floor numbers may be comparing one threshold-positive unit against one threshold-negative unit, with the threshold-positive one carrying a structurally higher resale value over a fifteen-year horizon.

Discontinuity two: the amenity floor

Most pre-construction towers in Miami place an amenity floor somewhere in the middle of the building. The spa, the gym, the pool deck, the restaurant, or some combination. The amenity floor is typically between the fifteenth and the twenty-fifth floor in a forty-story tower, though the position varies.

The units immediately above and below the amenity floor price differently than the rest. The units immediately above benefit from adjacency to the amenity without sharing a wall with the gym or the mechanical systems that serve it. They typically price at a one to two percent premium above the trend.

The units immediately below sit beneath the pool deck, the spa plumbing, or the restaurant kitchen. They typically price at a one to two percent discount against the trend. The discount funds the buyer's tolerance for the residual noise, vibration, or plumbing proximity that the amenity floor introduces.

A buyer who selects a unit immediately below the amenity floor without understanding the discount is paying the trend price for a discounted unit. A buyer who selects the unit immediately above without understanding the premium is paying a small amount more for a meaningfully different daily experience.

The discontinuity is mapped on the release sheet. The public list does not flag it.

Discontinuity three: the mechanical floor

In high-rise towers, the mechanical floor is the building's lung. Air handlers, water pumps, electrical switchgear, telecommunications. The mechanical floor is typically on or near a mid-tower band and is unoccupied. The floor above it is residential. The floor below it is residential.

The discount for the residential floor immediately above the mechanical floor is typically two to three percent. The discount funds the residual vibration and noise that propagates upward from the mechanical equipment, particularly the air handlers. The discount for the floor below is smaller, in the range of one percent, and funds the same effect propagating downward.

In some towers, the mechanical floor is intentionally vented in a way that minimizes the effect on adjacent residential floors. In others, it is not. The release sheet typically reflects the developer's internal assessment of the effect.

A buyer who selects an above-mechanical unit without the discount has paid the trend price for a sub-trend product. The seller's market in resale will eventually correct this, but the correction is realized by the second owner, not the first.

Discontinuity four: the penthouse band

The top five to eight floors of most Miami pre-construction towers break from the vertical pricing curve entirely. They are priced as a separate sub-product with their own square-foot rate, often forty to eighty percent above the floor immediately below the band.

The penthouse band is the developer's flagship product. The square footage per unit is larger. The ceiling heights are higher. The finishes are upgraded. The unit count per floor is lower. The amenities, in some buildings, are exclusive: a penthouse-band-only pool, lounge, or concierge.

The pricing inside the penthouse band is also not linear. The lowest penthouse-band floor typically prices at the lowest premium against the band's average. The top floor, the actual penthouse, prices at the highest premium, sometimes twice the band's average. The pattern reflects the developer's recognition that the top unit is its own product.

A buyer who is considering a penthouse band unit is operating in a different commercial reality than a buyer in the main building. The release sheet typically treats the band as a separate sub-document. The negotiation, the deposit schedule, and the assignment policy can all differ.

Discontinuity five: the unit-line preference

The five discontinuities above are vertical. The fifth is lateral. Two units on the same floor, of the same square footage, can price five to fifteen percent apart depending on which side of the building they face.

In Brickell, north-facing units with skyline exposure price above south-facing units with parking-deck or alley exposure. In Aventura, west-facing units with intracoastal exposure price above east-facing units with ocean exposure, because the buyer pool for Aventura prioritizes the protected-water view over the open-ocean view. In Miami Beach, ocean-facing units price above bay-facing units, but the relationship reverses in certain Sunny Isles towers where the bay exposure includes the marina infrastructure that the buyer pool values.

The release sheet maps the unit-line preference explicitly. The public list typically lists units by floor and unit number without flagging the preference. A buyer who selects a unit by floor number alone, without understanding the lateral pricing structure, is paying floor-trend prices on a unit-line that the developer's pricing model marks as discounted.

How a buyer uses this

A buyer who reads the release sheet sees the five discontinuities. The buyer can do three things with that information.

The buyer can choose the unit-line. Inside the Friends and Family window, the buyer can request a specific unit-line. The release sheet shows which lines are at premium and which are at discount. The buyer who selects a premium-priced line at trend pricing is paying below the line's structural value. The buyer who selects a discounted line at trend pricing is paying above the line's structural value. The release sheet is the only document that flags which is which.

The buyer can negotiate the floor. Inside the window, the floor premium is negotiable on specific units, particularly in the bands immediately above and below the discontinuities. A buyer can request a price at the trend rate on a unit that the release sheet would otherwise price at a premium, by exchanging a less-preferred unit-line or a longer deposit schedule.

The buyer can model the resale. The discontinuities persist into the resale market. A unit purchased with full awareness of which discontinuities applied to it produces a resale curve that matches the buyer's underwriting. A unit purchased at trend pricing on a discontinuity-affected position produces a resale curve that does not.

The release sheet is the document that contains the answers. It is the document that is not in the brochure, not on the website, and not in the sales gallery binder. It exists inside the brokerage firms that have earned a position on the developer's release list. That is the practical meaning of broker access in a pre-construction context. Welcome home.

End of article